What Is the Fisher Effect?

The Fisher effect, named after economist Irving Fisher, describes the relationship between nominal interest rates, real interest rates, and expected inflation. It states that the nominal interest rate equals the real rate adjusted for inflation. This calculator uses the exact Fisher equation to convert a real rate and an inflation rate into a nominal rate.

How to Use This Calculator

Enter the real interest rate (the inflation-adjusted return you expect) and the expected inflation rate, both as percentages. The calculator returns the nominal interest rate using the exact compounding formula, plus the common approximation for comparison.

The Formula Explained

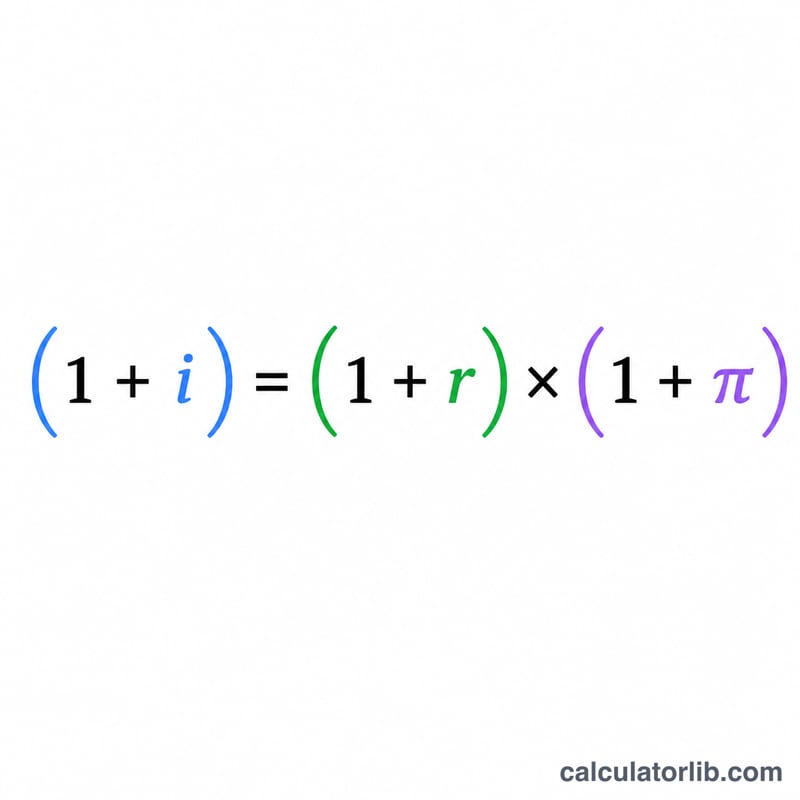

The exact relationship is $$(1 + i) = (1 + r)\times(1 + \pi)$$ where i is the nominal rate, r is the real rate, and \(\pi\) is the inflation rate. Solving for the nominal rate gives $$i = (1 + r)(1 + \pi) - 1$$ For small rates, this simplifies to the well-known approximation $$i \approx r + \pi$$ The difference between the two grows as rates rise, because the exact formula captures the cross-term \(r \times \pi\).

Worked Example

Suppose the real interest rate is 3% and expected inflation is 2%. The exact nominal rate is $$(1 + 0.03)(1 + 0.02) - 1 = 1.0506 - 1 = 0.0506$$ or 5.06%. The approximation gives \(3\% + 2\% = 5\%\). The small 0.06% gap is the cross-term \((0.03 \times 0.02)\).

FAQ

Why use the exact formula instead of just adding? The approximation \(r + \pi\) ignores the compounding cross-term and understates the nominal rate, especially when rates are high (e.g. during high inflation).

Can I solve for the real rate instead? Yes — rearrange to \(r = (1 + i)/(1 + \pi) - 1\). This calculator focuses on finding the nominal rate from real and inflation inputs.

Are negative rates allowed? Yes. You can enter negative real rates or deflation (negative inflation) and the formula still applies.