What Is Interest Rate Parity?

Interest Rate Parity (IRP) is a foundational concept in international finance that links exchange rates and interest rates between two countries. The theory of covered interest rate parity (CIRP) states that, in the absence of arbitrage, the difference between the forward and spot exchange rates must exactly offset the difference in interest rates between the two currencies. If this relationship did not hold, traders could borrow in the low-rate currency, convert and invest in the high-rate currency, and lock in a risk-free profit using a forward contract.

How to Use This Calculator

Enter the current spot exchange rate (units of domestic currency per one unit of foreign currency), the domestic interest rate, and the foreign interest rate, both as annual percentages. The calculator returns the theoretical no-arbitrage forward exchange rate, the forward/spot factor, and whether the foreign currency trades at a forward premium or discount.

The Formula Explained

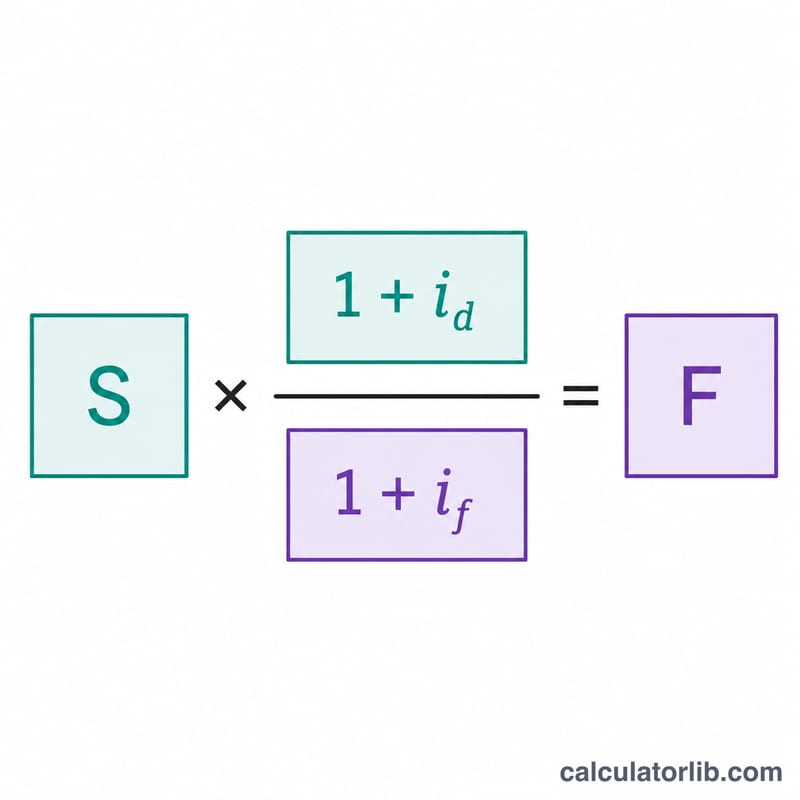

The forward rate is computed as:

$$F = \text{Spot} \times \frac{1 + \dfrac{\text{Domestic Rate (\%)}}{100}}{1 + \dfrac{\text{Foreign Rate (\%)}}{100}}$$

Here \(S\) is the spot rate, \(i_d\) is the domestic interest rate, and \(i_f\) is the foreign interest rate (both expressed as decimals). When the domestic rate exceeds the foreign rate, the forward rate rises above the spot rate, so the foreign currency trades at a forward premium.

Worked Example

Suppose the spot rate is 1.20, the domestic interest rate is 5%, and the foreign interest rate is 3%. The factor is $$\frac{1.05}{1.03} = 1.019417.$$ The forward rate is $$1.20 \times 1.019417 = \mathbf{1.223301},$$ a forward premium of about 1.94%.

FAQ

What is the difference between covered and uncovered IRP? Covered IRP uses a forward contract to hedge currency risk, making it an arbitrage condition. Uncovered IRP relies on expected future spot rates and does not require a forward contract.

Why might real markets deviate from IRP? Transaction costs, capital controls, counterparty credit risk, and differences in instrument liquidity can cause small, persistent deviations.

How should I quote the spot rate? Use domestic currency per unit of foreign currency so the forward rate output uses the same convention.