What This Calculator Does

The Life Insurance Premium Calculator gives you a quick, ballpark estimate of what a term life insurance policy might cost. It combines your chosen coverage amount, policy term, age, gender, and smoker status with a base rate per $1,000 of cover to produce annual, monthly, and total-over-term premium figures. It is a planning tool — actual insurer quotes depend on full underwriting, medical history, occupation, and country-specific pricing.

How to Use It

Enter the coverage (sum assured) you want, the number of years you want to be covered, your current age, and the base rate your insurer quotes per $1,000 of coverage each year (commonly $0.50–$3.00 for healthy adults). Select your gender and whether you smoke, then read off your estimated annual and monthly premiums.

The Formula Explained

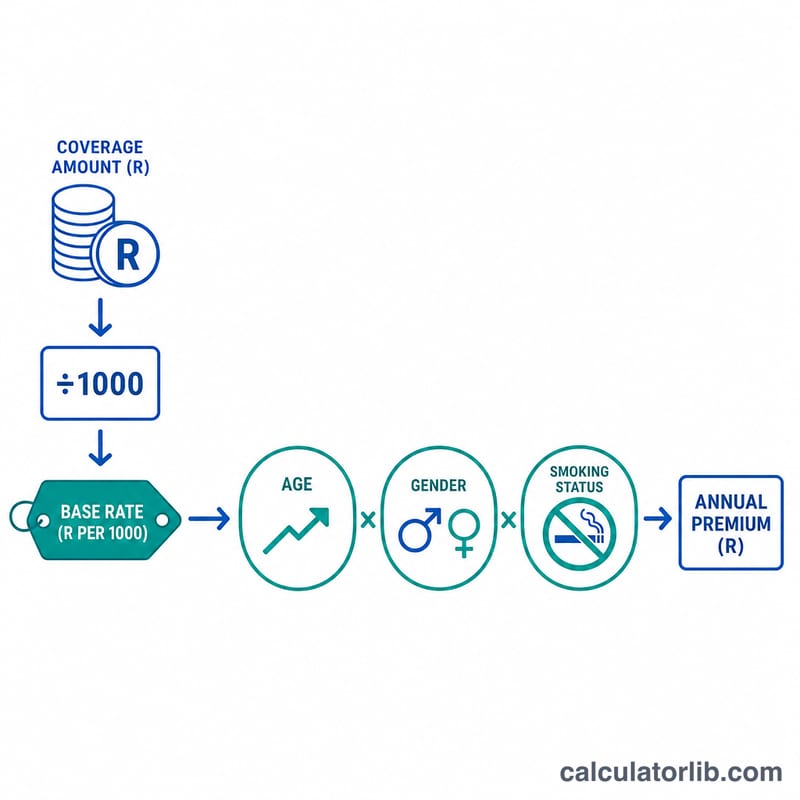

The core premium is \(\frac{\text{Coverage}}{1000} \times \text{Rate}\). This is then multiplied by a risk multiplier built from three loadings: an age factor that adds 3% per year above age 30, a gender factor (0.90 for females reflecting lower average mortality), and a smoker factor of 1.75 for smokers. The monthly premium is the annual figure divided by 12, and the total paid is the annual premium times the policy term.

$$\text{Annual Premium} = \frac{\text{Coverage}}{1000} \times \text{Rate} \times R$$

$$\text{where}\quad \left\{ \begin{aligned} R &= A \times G \times S \\ A &= 1 + \max\!\left(0,\ \text{Age} - 30\right)\times 0.03 \\ G &= \begin{cases} 0.90 & \text{Female} \\ 1.00 & \text{otherwise} \end{cases} \\ S &= \begin{cases} 1.75 & \text{Smoker} \\ 1.00 & \text{otherwise} \end{cases} \end{aligned} \right.$$

Worked Example

Suppose you want $500,000 of cover for 20 years, you are a 35-year-old non-smoking male, and the base rate is $1.50 per $1,000. The age factor is \(1 + 0.03 \times (35 - 30) = 1.15\), gender 1.0, smoker 1.0, so the multiplier is 1.15. Annual premium:

$$\frac{500000}{1000} \times 1.50 \times 1.15 = 500 \times 1.50 \times 1.15 = \mathbf{\$862.50}$$

Monthly = $71.88, and total over 20 years = $17,250.

FAQ

Is this an actual quote? No — it is an educational estimate. Insurers use detailed actuarial tables and medical underwriting.

Why does smoking raise the price so much? Smokers have materially higher mortality risk, so this tool applies a 1.75× loading, in line with typical industry practice.

What base rate should I use? If you do not have a quote, try $1–$2 per $1,000 for a healthy adult; older or higher-risk applicants pay more.