What this calculator does

This tool estimates how much interest you save by moving a loan from a higher interest rate to a lower one. It assumes a standard fully amortizing loan (like a mortgage, auto loan, or personal loan) with fixed monthly payments over the same term, and reports the difference in total interest paid between the two rates.

How to use it

Enter your loan amount, your current annual interest rate (APR), the new lower rate you are considering, and the loan term in years. The calculator computes the monthly payment at each rate, multiplies by the number of months to get the total paid, subtracts the principal to isolate interest, and then shows the difference. It also displays your monthly payment savings.

The formula explained

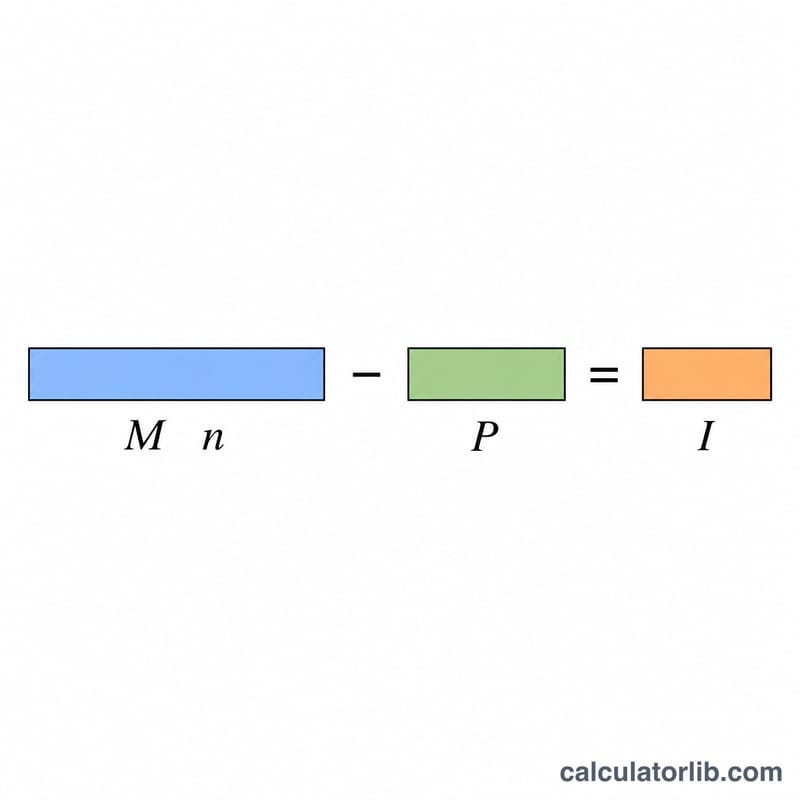

The monthly payment is \(M = P\cdot r / (1 - (1 + r)^{-n})\), where P is the principal, r is the monthly rate (annual rate ÷ 12 ÷ 100), and n is the total number of monthly payments. Total interest at a given rate is the sum of all payments minus the principal: \(I = M\cdot n - P\). Savings equals the interest at the higher rate minus the interest at the lower rate.

$$M = P\cdot \frac{r}{1-(1+r)^{-n}}$$

Worked example

A $200,000 loan over 30 years (360 months) at 6.5% has a monthly payment of about $1,264.14, for total interest of roughly $255,089. At 5.5% the payment is about $1,135.58, for total interest of roughly $208,809. The interest savings is about $46,280, with monthly savings near $128.56.

$$\text{Savings} = (1{,}264.14 - 1{,}135.58)\cdot 360 \approx \$46{,}280$$FAQ

Does this assume I keep the same term? Yes. Both rates are amortized over the same term you enter, so this isolates the effect of the rate alone.

Does it include refinancing fees? No. It shows gross interest savings only — subtract closing costs or points to estimate net savings.

What if the rates are equal? Savings will be zero, since identical rates over the same term produce identical interest.