What Is Diluted EPS?

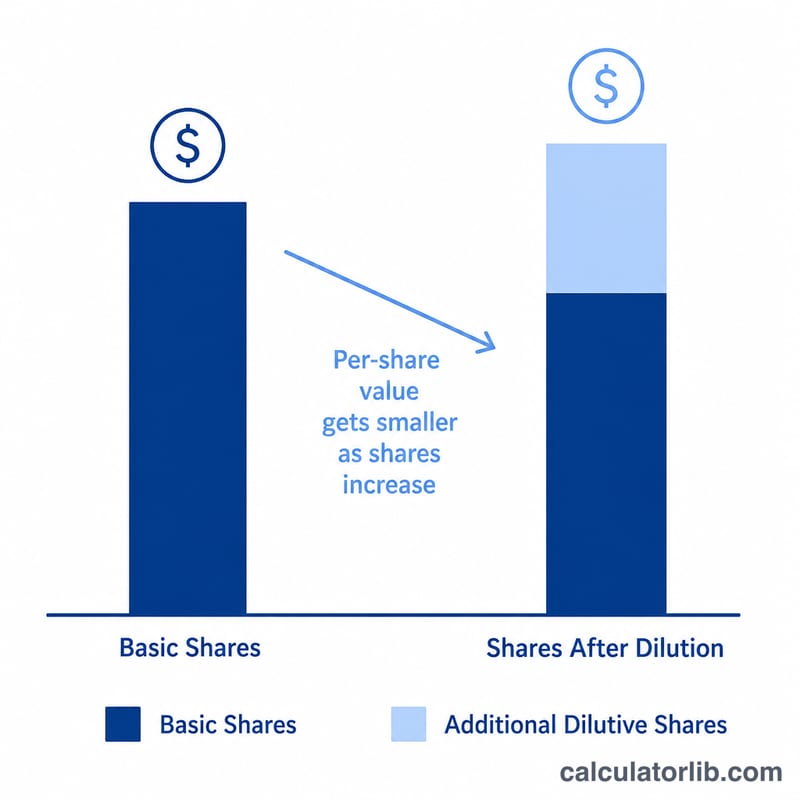

Diluted earnings per share (EPS) measures a company's profit allocated to each share of common stock, assuming all dilutive securities — stock options, warrants, convertible bonds, and convertible preferred shares — are exercised or converted into common stock. Because it expands the share count, diluted EPS is always equal to or lower than basic EPS, giving investors a more conservative, "worst-case" view of per-share profitability.

How to Use This Calculator

Enter four figures from the income statement and notes: net income, preferred dividends paid, the weighted average number of common shares outstanding, and the additional shares that would be created by dilutive securities. The calculator returns diluted EPS along with basic EPS and the percentage of dilution so you can see how much potential conversion erodes each shareholder's slice of earnings.

The Formula Explained

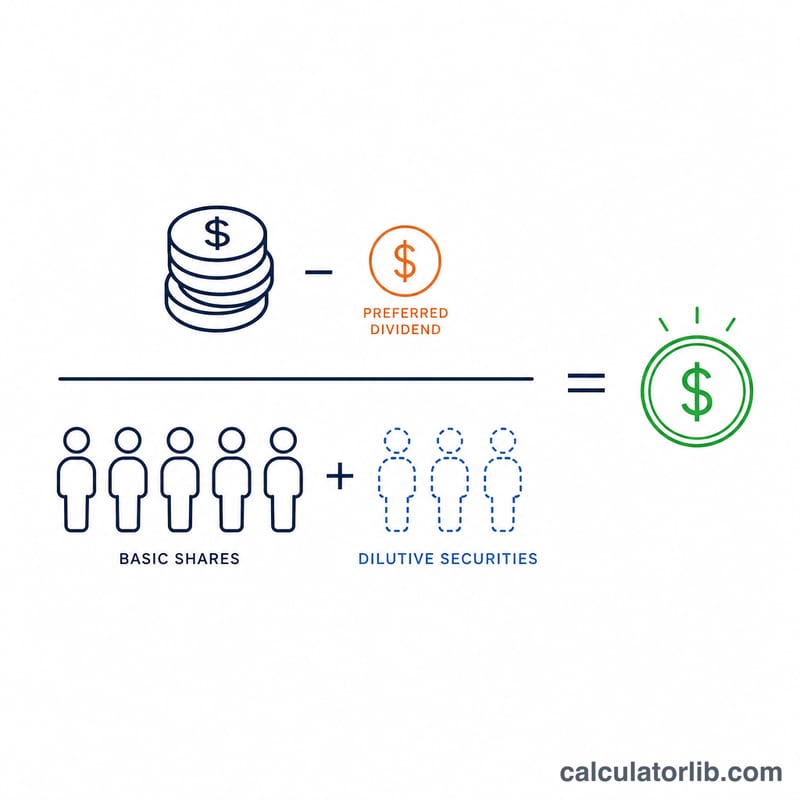

The numerator, Net Income − Preferred Dividends, is the earnings actually available to common shareholders, since preferred holders are paid first. The denominator adds the dilutive securities to the weighted average common shares. Dividing the two gives the diluted EPS.

$$\text{Diluted EPS} = \frac{\text{Net Income} - \text{Preferred Dividends}}{\text{Weighted Avg Shares} + \text{Dilutive Securities}}$$

Worked Example

Suppose a company reports net income of $1,000,000, pays $50,000 in preferred dividends, has 400,000 weighted average common shares, and 100,000 shares from dilutive options. Earnings to common = \(\$1{,}000{,}000 - \$50{,}000 = \$950{,}000\). Total diluted shares = \(400{,}000 + 100{,}000 = 500{,}000\). Diluted EPS:

$$\text{Diluted EPS} = \frac{\$950{,}000}{500{,}000} = \mathbf{\$1.90}$$Basic EPS = \(\$950{,}000 \div 400{,}000 = \$2.375\), so dilution reduces EPS by about 20%.

FAQ

Why is diluted EPS lower than basic EPS? Because it assumes more shares exist, spreading the same earnings across a larger base.

What counts as a dilutive security? Stock options, warrants, convertible debt, and convertible preferred stock that would increase the common share count if exercised or converted. Anti-dilutive instruments (those that would raise EPS) are excluded.

Where do I find these numbers? Net income and preferred dividends come from the income statement; the weighted average and dilutive share counts are disclosed in the EPS note of the financial statements.