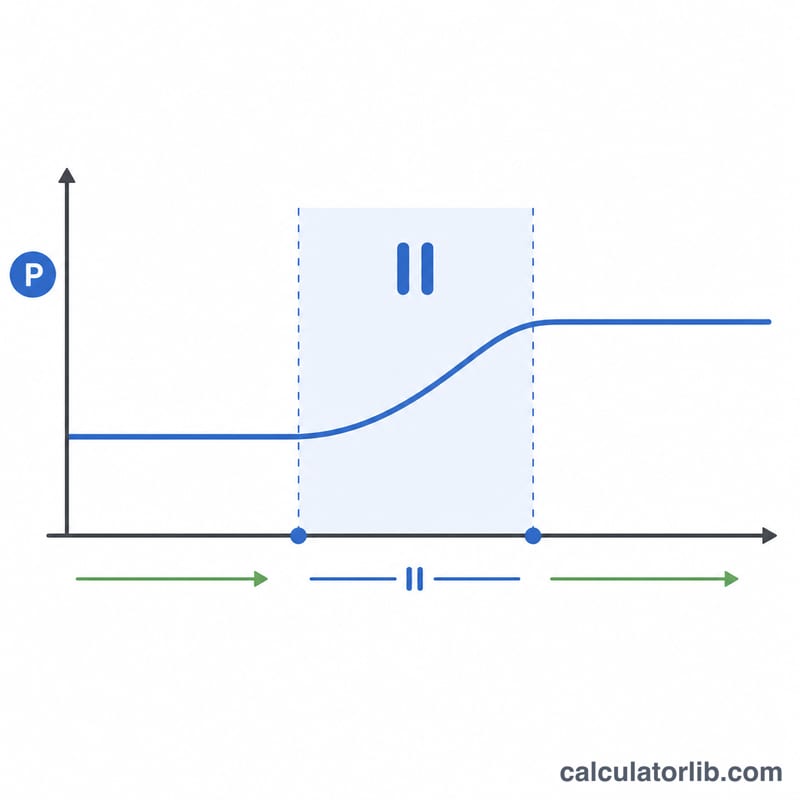

What Is a Loan Moratorium Calculator?

A loan moratorium is a temporary pause on your EMI payments, often granted during financial hardship or relief schemes. While you skip payments, interest usually keeps accruing on the outstanding balance and gets compounded. This calculator shows exactly how much your loan balance grows during the moratorium and what your revised monthly instalment (EMI) will be afterward.

How to Use It

Enter your outstanding loan amount, the annual interest rate, the length of the moratorium in months, and the remaining tenure after the moratorium ends. The tool first compounds the balance over the pause period, then recomputes a fresh EMI so the new balance is cleared over the remaining months.

The Formula Explained

The monthly rate is \(r = \text{annual rate} \div 12 \div 100\). During the moratorium, no payment is made, so the balance grows as $$B = P \times (1 + r)^m$$ where m is the number of moratorium months. The revised EMI is then the standard amortisation formula applied to B over the remaining tenure n: $$EMI = \frac{B \cdot r \cdot (1+r)^n}{(1+r)^n - 1}$$

Worked Example

Suppose you owe ₹500,000 at 9% annual interest, take a 6-month moratorium, and have 120 months left. The monthly rate is 0.0075. The accrued balance is $$500{,}000 \times (1.0075)^6 \approx ₹522{,}941$$ Spreading this over 120 months gives a revised EMI of about ₹6,624 per month.

FAQ

Does interest really accrue during a moratorium? In most cases yes — a moratorium defers payment, not interest. The unpaid interest is added to the principal and compounds.

Why does my EMI go up? Because the balance is larger after the moratorium, and (if tenure is unchanged) the bank must recover more over the same period.

Can I keep my old EMI instead? Some lenders let you extend the tenure rather than raise the EMI. This tool assumes a fixed remaining tenure; adjust the tenure field to compare.