What Is Operating Cash Flow?

Operating Cash Flow (OCF) measures the cash a business generates from its core operations during a period. Unlike net income, which includes non-cash items and accrual timing, OCF shows the actual cash moving through the business — a key signal of financial health and the ability to fund operations, pay debt, and reinvest. This calculator uses the indirect method, the most common approach on the statement of cash flows.

How to Use This Calculator

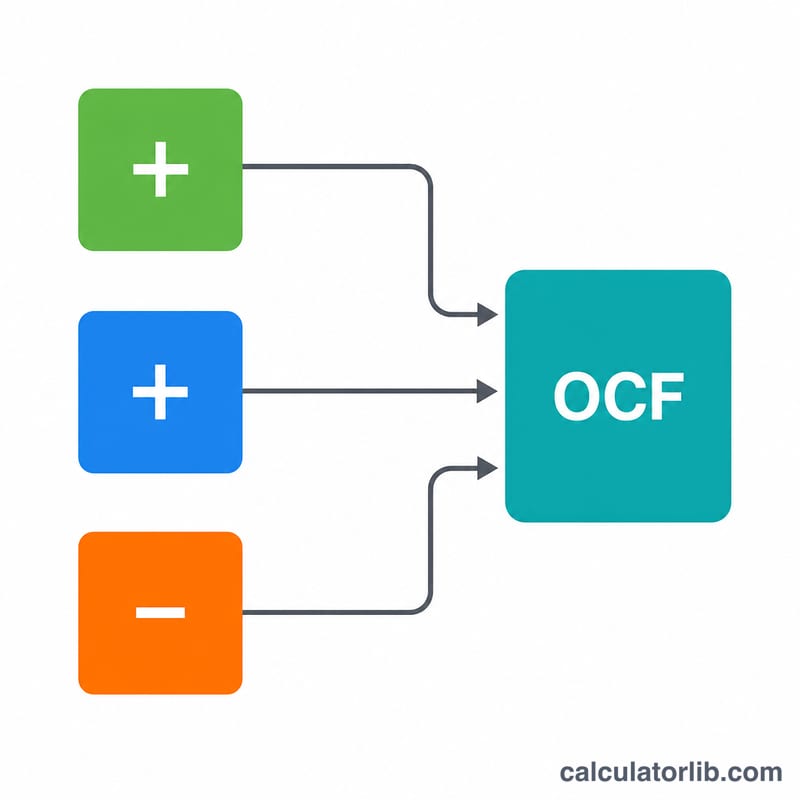

Enter three figures pulled from your financial statements: Net Income from the income statement, Non-Cash Expenses (such as depreciation and amortization added back), and the Change in Working Capital (current operating assets minus current operating liabilities for the period). The tool instantly returns your operating cash flow.

The Formula Explained

$$\text{OCF} = \text{Net Income} + \text{Non-Cash Expenses} - \text{Change in Working Capital}$$ Non-cash expenses like depreciation reduced net income but never used cash, so they are added back. An increase in working capital (e.g., more inventory or receivables) ties up cash, so it is subtracted; a decrease frees cash and increases OCF. If your working capital figure represents a decrease, enter it as a negative number.

Worked Example

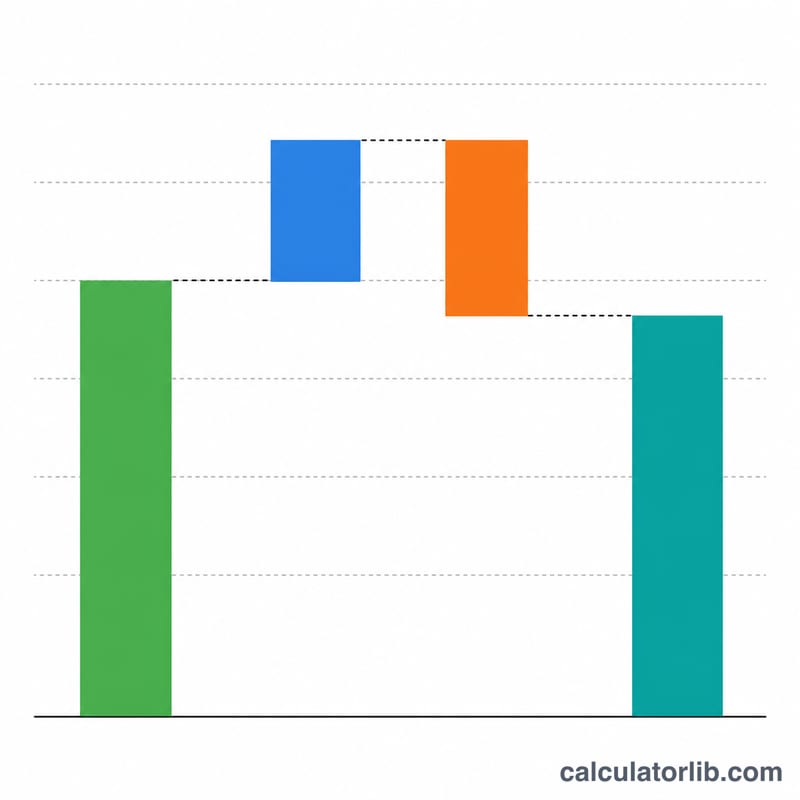

A company reports net income of $100,000, depreciation and other non-cash expenses of $20,000, and a working capital increase of $15,000. $$\text{OCF} = 100{,}000 + 20{,}000 - 15{,}000 = \mathbf{\$105{,}000}$$ The business generated $105,000 in cash from operations despite reporting $100,000 in net income.

FAQ

What counts as a non-cash expense? Depreciation, amortization, stock-based compensation, and deferred taxes are common examples.

Why subtract change in working capital? Growing inventory or receivables consumes cash even when revenue is recorded, so an increase reduces cash flow.

Can OCF be negative? Yes — a negative result means operations consumed more cash than they produced, which may signal trouble if sustained.