What Is Free Cash Flow to Firm (FCFF)?

Free Cash Flow to Firm (FCFF), also called unlevered free cash flow, is the cash a business generates from operations that is available to all capital providers — both debt holders and equity holders — after accounting for taxes, reinvestment in fixed assets, and changes in working capital. It is the cornerstone input for enterprise-value DCF valuation, because it is measured before the effect of financing (interest payments).

How to Use This Calculator

Enter five figures from a company's income statement and cash flow statement: operating profit (EBIT), the effective tax rate as a percentage, depreciation & amortization (D&A), capital expenditures (CapEx), and the change in net working capital (ΔNWC). The calculator returns FCFF along with a breakdown of each component so you can see exactly how the number was built.

The Formula Explained

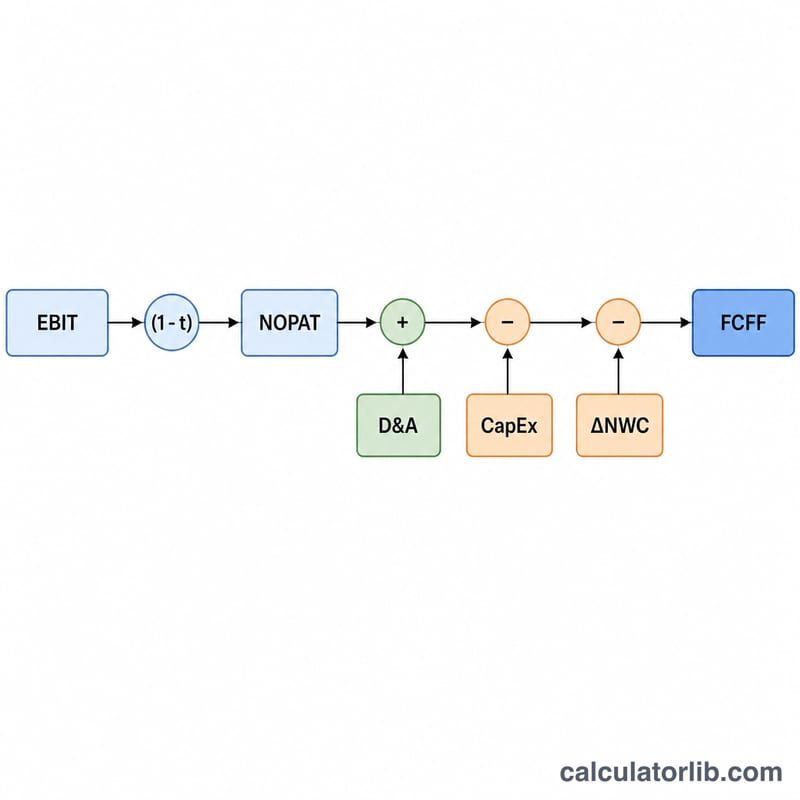

$$\text{FCFF} = \text{EBIT} \times \left(1 - \frac{\text{Tax Rate}}{100}\right) + \text{D\&A} - \text{CapEx} - \Delta\text{NWC}$$ We start with EBIT and tax it to get NOPAT (net operating profit after tax). D&A is added back because it is a non-cash expense that reduced EBIT. CapEx is subtracted because building and replacing assets consumes cash. Finally, an increase in net working capital (more inventory or receivables) ties up cash, so a positive ΔNWC is subtracted.

Worked Example

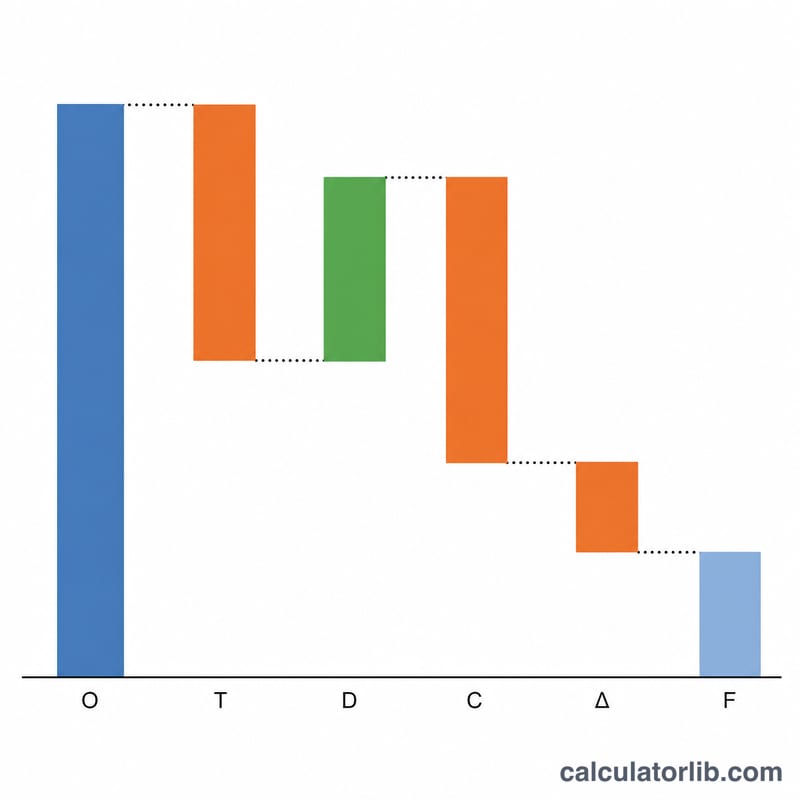

Suppose EBIT = $1,000,000, tax rate = 25%, D&A = $200,000, CapEx = $300,000 and ΔNWC = $50,000. \(\text{NOPAT} = 1{,}000{,}000 \times 0.75 = \$750{,}000\). $$\text{FCFF} = 750{,}000 + 200{,}000 - 300{,}000 - 50{,}000 = \$600{,}000$$

FAQ

What is the difference between FCFF and FCFE? FCFF is unlevered (before financing) and is owed to all investors; FCFE (Free Cash Flow to Equity) subtracts after-tax interest and net debt repayments, leaving cash for equity holders only.

Why subtract change in net working capital? Growing receivables and inventory consume cash even though they are not expenses, so the increase must be deducted to reflect true cash generation.

What if ΔNWC is negative? A decrease in working capital releases cash; enter a negative number and FCFF will rise accordingly.