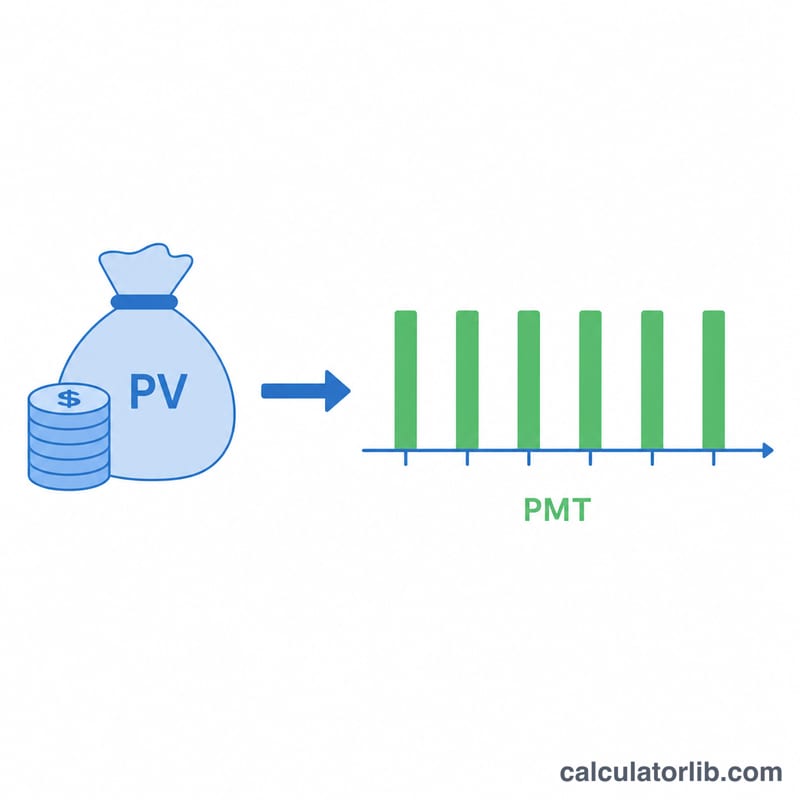

What This Calculator Does

The Annuity Payout From Lump Sum Calculator tells you how large a regular payment a single upfront sum can sustain over a chosen number of years, assuming the remaining balance keeps earning interest. It is useful for retirement planning, structured settlements, or converting savings into a predictable income stream.

How to Use It

Enter your lump sum (present value), the annual interest rate the funds will earn, the payout period in years, and how often you want to receive payments (weekly, monthly, quarterly, or annually). The calculator returns the payment per period along with the total amount paid out and the total interest earned over the life of the annuity.

The Formula Explained

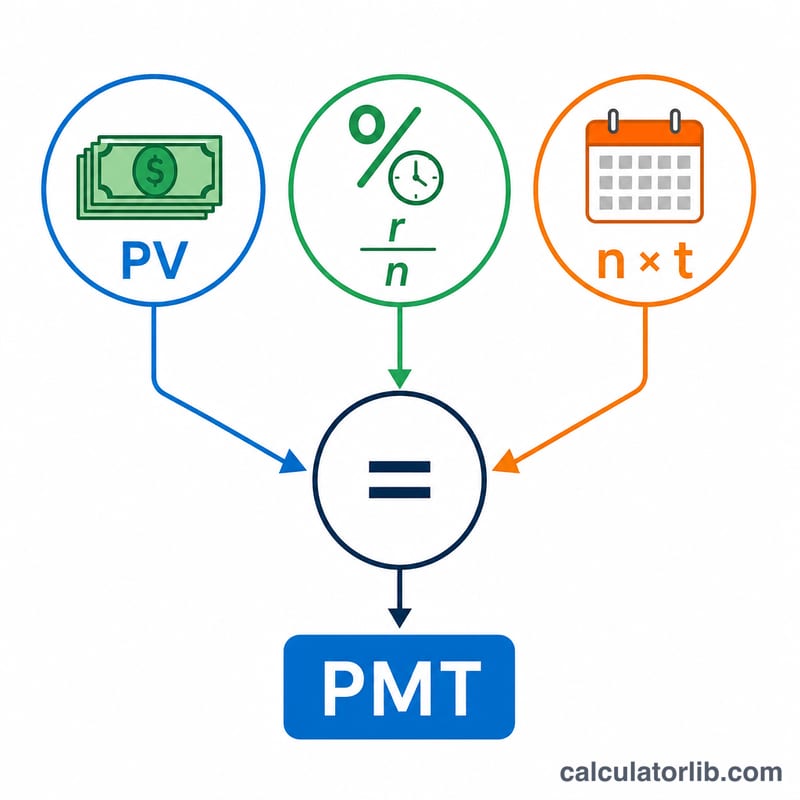

The payment is found with the ordinary annuity present-value formula solved for PMT:

$$PMT = \frac{PV \cdot (r/n)}{1-(1+r/n)^{-n\cdot t}}$$

Here r is the annual rate as a decimal, n is payments per year, and t is the number of years. The factor \(r/n\) converts the annual rate to a per-period rate, while the denominator discounts all future payments back to today's value.

Worked Example

Suppose you invest a $500,000 lump sum at 5% annual interest and want monthly payments for 20 years. Then \(i = 0.05/12 \approx 0.0041667\) and the number of payments is 240. The denominator is \(1 - (1.0041667)^{-240} \approx 0.631226\), so $$PMT = \frac{500{,}000 \times 0.0041667}{0.631226} \approx \$3{,}299.78 \text{ per month}.$$ Over 240 payments that totals about $791,948, of which roughly $291,948 is interest.

Key Terms Defined

- Present value (PV) — the lump sum you start with today, i.e. the amount being converted into a stream of payments.

- Annual interest rate (r) — the yearly rate of return assumed on the remaining balance, entered as a percentage (e.g. 5 means 5%).

- Payments per year (n, frequency) — how often a payment is made: 12 (monthly), 4 (quarterly), 52 (weekly) or 1 (annually).

- Term (t) — the number of years over which payments are made. The total number of payments is \(n \cdot t\).

- Periodic rate (r/n) — the interest rate applied to each period, found by dividing the annual rate by the number of periods per year. For 6% paid monthly this is \(0.06/12 = 0.005\) per month.

- Ordinary annuity — payments occur at the end of each period. The formula on this page assumes an ordinary annuity.

- Annuity due — payments occur at the beginning of each period; each payment is slightly smaller than the ordinary case for the same lump sum, by a factor of \((1+i)\).

- Total interest earned — the sum of all payments minus the original lump sum: \((PMT \cdot n \cdot t) - PV\). It reflects the growth on the balance that has not yet been paid out.

Interpreting Your Result

The periodic payment is the fixed amount you would receive each period (monthly, quarterly, weekly or annually) for the entire term. It is calculated so that the lump sum, plus the interest it earns along the way, is paid out evenly.

The total paid is that payment multiplied by the number of periods — the cumulative cash you receive over the whole term. The interest earned is the portion of the total paid that comes from growth on the balance rather than from your original principal.

By design, the account balance is fully depleted to zero at the end of the term: the formula amortizes the entire lump sum plus interest, leaving nothing behind. If you want the principal to last indefinitely, you would instead withdraw only the interest (a perpetuity), which produces smaller payments.

Two relationships drive the result: a higher interest rate raises each payment (more growth to distribute), and a shorter term raises each payment (the same principal is spread over fewer periods). Conversely, lower rates or longer terms reduce each payment.

These figures are pre-tax, pre-fee and pre-inflation illustrations based on a constant assumed rate. Actual payouts may differ due to taxes, administrative or insurance charges, variable returns, and the eroding effect of inflation on purchasing power. This is general educational information, not financial advice — consult a qualified professional before making decisions about your own money.

FAQ

Does this assume payments at the end of each period? Yes — it uses an ordinary annuity (payments in arrears). An annuity due (payments at the start) would yield slightly smaller payments.

What if I enter a 0% interest rate? The calculator simply divides the lump sum evenly across all periods.

Are taxes or fees included? No. Results are pre-tax and ignore management fees or inflation; treat them as an illustration, not financial advice.