What This Calculator Does (US Only)

This tool is for U.S. business owners considering an S-Corporation election. As a sole proprietor or single-member LLC, your entire net profit is subject to 15.3% self-employment (SE) tax — 12.4% Social Security (up to the annual wage base) and 2.9% Medicare. With an S-Corp, you pay yourself a "reasonable salary" subject to payroll tax, and the remaining profit is taken as a distribution that escapes that 15.3% tax. This calculator estimates how much SE/payroll tax you save. Figures use the 2024 Social Security wage base of $168,600 as a default; update it for your tax year.

How to Use It

Enter your business net profit, the reasonable salary you intend to pay yourself, and the Social Security wage base for the year. The calculator computes the distribution (profit minus salary) and the tax saved on that distribution.

The Formula Explained

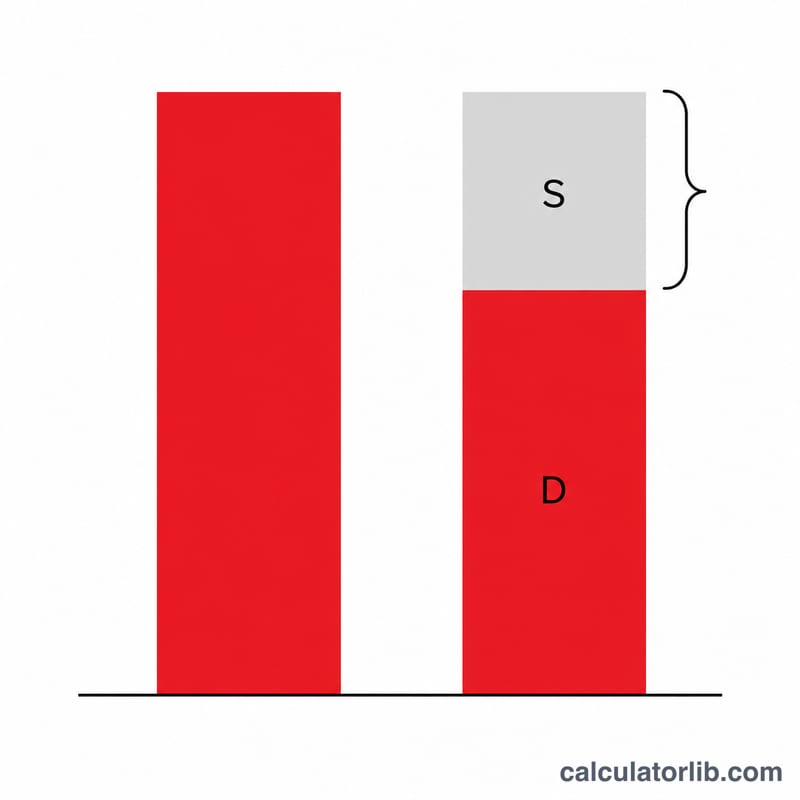

Distribution \(D = \text{Profit} - \text{Salary}\). Social Security tax (12.4%) only applies up to the wage base \(B\), and your salary already consumes part of that base, so only \(\min(D,\, B - S)\) of the distribution would have been hit by SS tax. Medicare (2.9%) has no cap, so it applies to the entire distribution.

$$\text{Total saved} = \min(D,\, B - S) \times 12.4\% + D \times 2.9\%$$

Worked Example

Profit $120,000, salary $60,000, wage base $168,600. Distribution = $60,000. SS room remaining = \(\$168{,}600 - \$60{,}000 = \$108{,}600\), so all $60,000 is below the cap: SS saved = \(\$60{,}000 \times 12.4\% = \$7{,}440\). Medicare saved = \(\$60{,}000 \times 2.9\% = \$1{,}740\). Total SE tax saved = $9,180 per year.

FAQ

What is a "reasonable salary"? The IRS requires S-Corp owner-employees to take a salary comparable to what similar work would earn. Setting it too low to dodge tax is a common audit trigger.

Does this account for income tax? No — distributions still face ordinary income tax. This tool only estimates SE/payroll (Social Security + Medicare) tax savings.

Are there extra costs to an S-Corp? Yes: payroll processing, additional tax filings, and state fees. Weigh these against the savings shown here.