What This Calculator Does

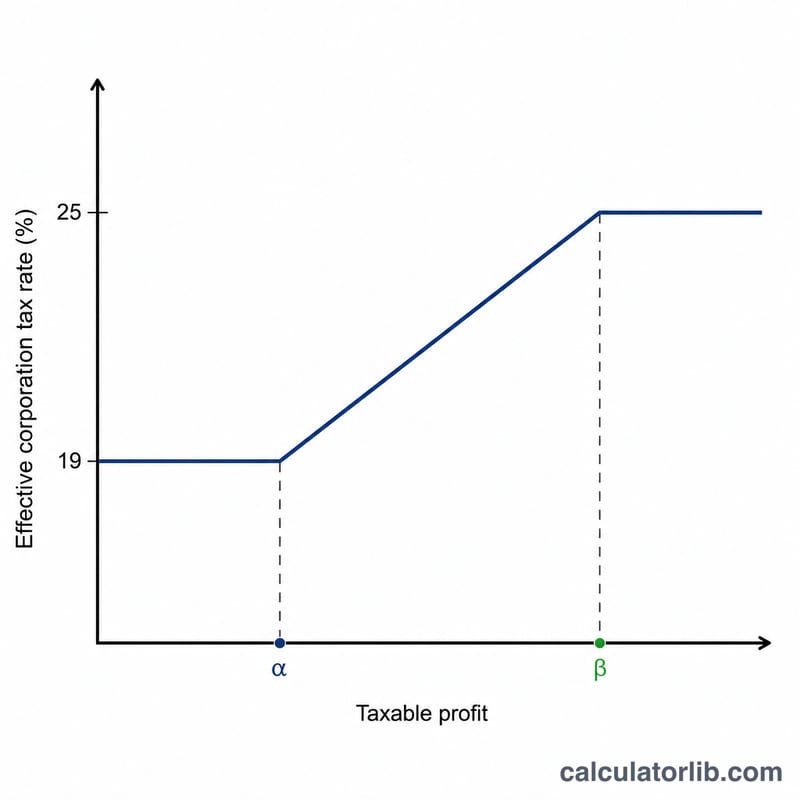

This tool applies to the United Kingdom and calculates Corporation Tax for accounting periods from 1 April 2023 onwards (Financial Year 2023 and later). From that date the UK uses a two-rate system: a small profits rate of 19% on profits up to £50,000, a main rate of 25% on profits of £250,000 or more, and marginal relief that smooths the jump between the two limits.

How to Use It

Enter your company's taxable profit for the period and the number of associated companies (companies under common control). The lower and upper limits (£50,000 and £250,000) are divided equally between you and any associated companies, so more associated companies push you into the higher-tax band sooner. The calculator returns the tax due, any marginal relief, profit after tax and your effective tax rate.

The Formula Explained

When profit (P) falls between the lower limit (L) and upper limit (U), tax is the main rate charge less marginal relief:

$$\text{Tax} = P \times 25\% - (U - P) \times \frac{3}{200}$$

The fraction \(\frac{3}{200}\) (0.015) is the standard marginal relief fraction. Below L the rate is a flat 19%; at or above U it is a flat 25%.

Worked Example

A company with £100,000 profit and no associated companies: gross tax = \(\pounds100{,}000 \times 25\% = \pounds25{,}000\). Marginal relief:

$$(\pounds250{,}000 - \pounds100{,}000) \times \frac{3}{200} = \pounds150{,}000 \times 0.015 = \pounds2{,}250$$Tax due = \(\pounds25{,}000 - \pounds2{,}250 = \) £22,750, an effective rate of 22.75%.

FAQ

What are associated companies? Companies that one controls another, or that are under common control. They share the £50k/£250k limits, reducing each company's threshold.

Why is my effective rate between 19% and 25%? Marginal relief tapers tax so the rate rises gradually across the £50k–£250k band rather than jumping.

Is this an official HMRC figure? This is an estimate for guidance. Always confirm with HMRC or an accountant before filing.