What Is the Gordon Growth Model?

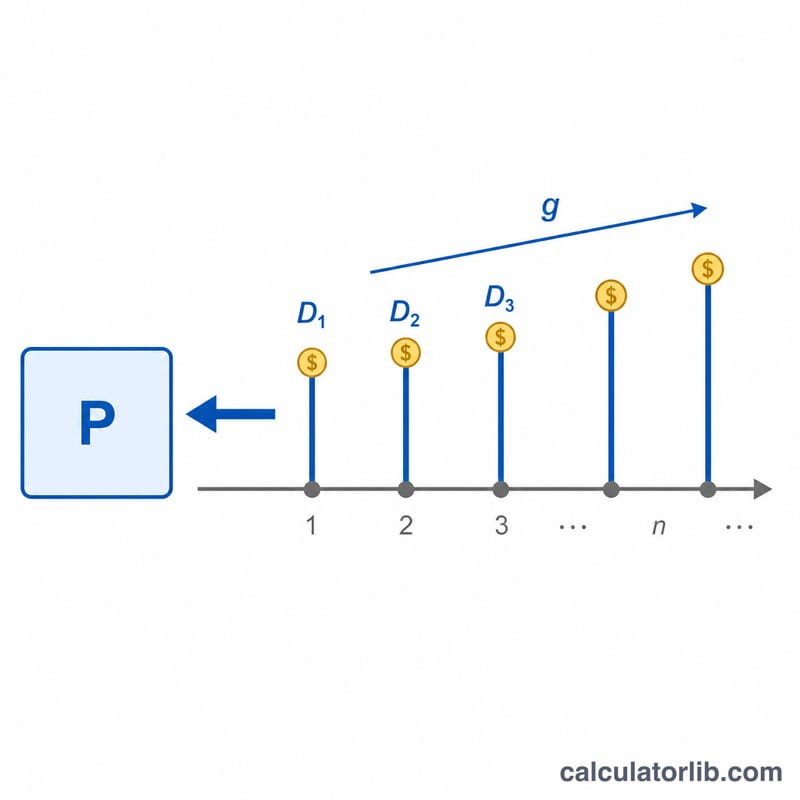

The Gordon Growth Model (GGM), also called the constant-growth Dividend Discount Model, estimates the intrinsic value of a stock that pays dividends expected to grow at a steady rate forever. It is one of the most widely used tools in fundamental equity valuation because it distills a company's worth down to three inputs: its current dividend, the required rate of return, and the long-term dividend growth rate.

How to Use This Calculator

Enter the current annual dividend per share (D0), your required rate of return (r) as a percentage, and the expected long-term dividend growth rate (g) as a percentage. The calculator grows the dividend one year forward to get D1, then divides it by the spread between r and g to produce the estimated fair price per share. Note that the model only works when r is greater than g — otherwise the result is undefined or negative.

The Formula Explained

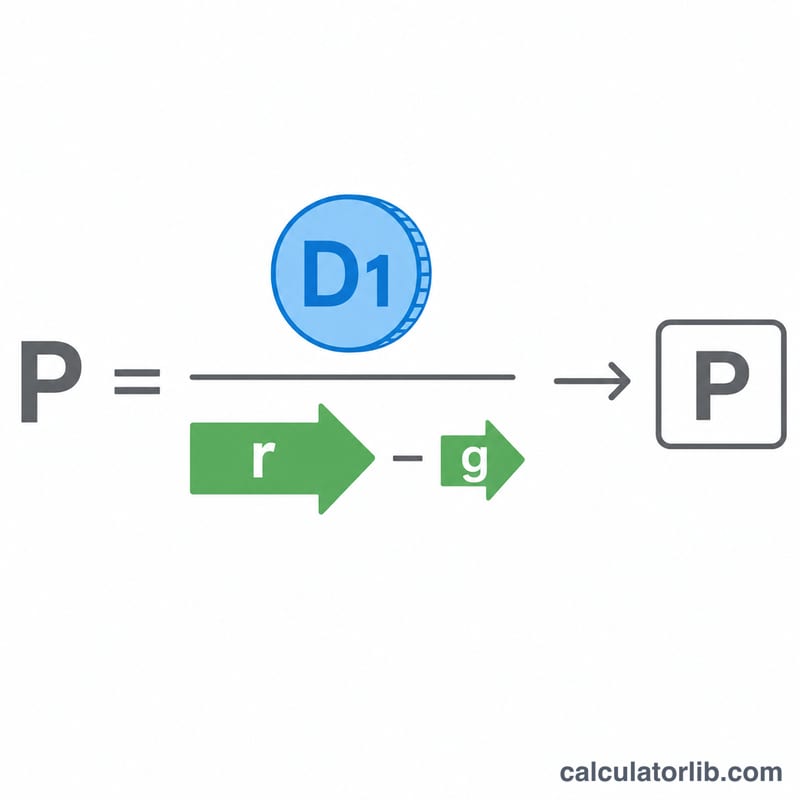

The core equation is \(P = D_1 / (r - g)\), where \(D_1 = D_0 \times (1 + g)\). P is the present value of an infinite stream of dividends growing at rate g, discounted at rate r. The denominator \((r - g)\) is the "spread"; the smaller it is, the more sensitive the valuation becomes, which is why small changes in growth assumptions can swing the price dramatically.

$$P = \frac{\text{Dividend } D_0 \times \left(1 + \frac{\text{Growth } g\,(\%)}{100}\right)}{\dfrac{\text{Return } r\,(\%)}{100} - \dfrac{\text{Growth } g\,(\%)}{100}}$$

Worked Example

Suppose a company currently pays a $2.00 annual dividend (D0), you require an 8% return (r), and you expect dividends to grow 3% per year (g). First, \(D_1 = 2.00 \times (1 + 0.03) = \$2.06\). Then $$P = \frac{2.06}{0.08 - 0.03} = \frac{2.06}{0.05} = \$41.20$$ per share. If the stock trades below $41.20, the model suggests it may be undervalued.

FAQ

Why must r be greater than g? If growth equals or exceeds the required return, the denominator is zero or negative and the model breaks down, implying infinite value — which is unrealistic for any real company.

What growth rate should I use? Use a sustainable long-term rate, typically no higher than the economy's nominal growth (often 2–5%). High short-term growth rates overstate value.

Does it work for non-dividend stocks? No. The GGM requires dividends. For companies that don't pay dividends, use discounted free cash flow models instead.