What Is Bond Convexity?

Convexity measures the curvature in the relationship between a bond's price and its yield. While duration gives a first-order (linear) estimate of how price moves when yields change, convexity adds the crucial second-order correction. Bonds with higher convexity are less sensitive to rising rates and gain more when rates fall — a desirable property for fixed-income investors. This calculator computes both the bond's fair price and its annualized convexity.

How to Use the Calculator

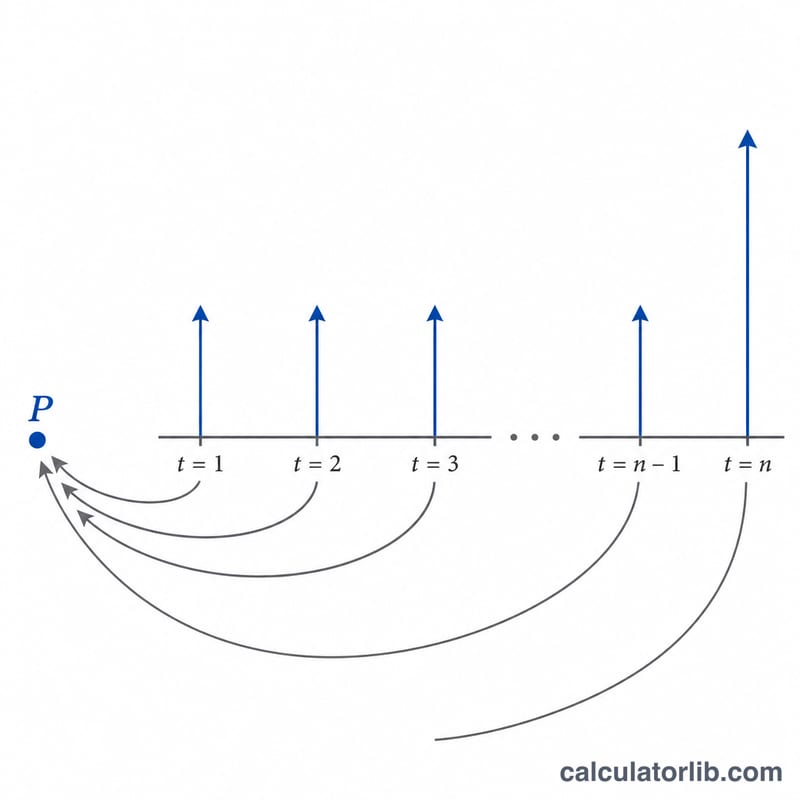

Enter the bond's face (par) value, its annual coupon rate, the yield to maturity, the number of years until maturity, and how many coupon payments are made per year. The tool discounts every cash flow, sums the convexity-weighted terms, and reports convexity in years². It also shows the present value (price) of the bond as a useful by-product.

The Formula Explained

For each period t, the cash flow \(CF_t\) (a coupon, plus the face value at maturity) is multiplied by \(t(t+1)\) and discounted by \((1+y)^{t}\), where \(y\) is the periodic yield. That sum is divided by the price times \((1+y)^{2}\). Because the math is done per period, we divide by the squared payment frequency \(m^{2}\) to express convexity in years.

$$C = \frac{1}{P\,(1+y)^{2}} \sum_{t=1}^{n} \frac{CF_t \cdot t\,(t+1)}{(1+y)^{t}} \cdot \frac{1}{k^{2}}$$ $$\text{where}\quad \left\{ \begin{aligned} k &= \text{Payments / Year} \\ y &= \dfrac{\text{YTM (\%)}/100}{k} \\ n &= \text{Years} \times k \\ CF_t &= \dfrac{\text{Face} \times \text{Coupon (\%)}/100}{k} \;(+\,\text{Face}\text{ if }t=n) \\ P &= \sum_{t=1}^{n} \dfrac{CF_t}{(1+y)^{t}} \end{aligned} \right.$$

Worked Example

Consider a $1,000 bond with a 5% annual coupon paid annually, an 8% yield, and 2 years to maturity. Cash flows: $50 at year 1 and $1,050 at year 2. Price = \(50/1.08 + 1050/1.08^{2} \approx \$946.50\). Convexity sum = \(50\cdot1\cdot2/1.08 + 1050\cdot2\cdot3/1.08^{2} = 92.59 + 5401.23 = 5493.82\). Convexity = \(5493.82 / (946.50 \times 1.08^{2}) \approx 4.98\) years².

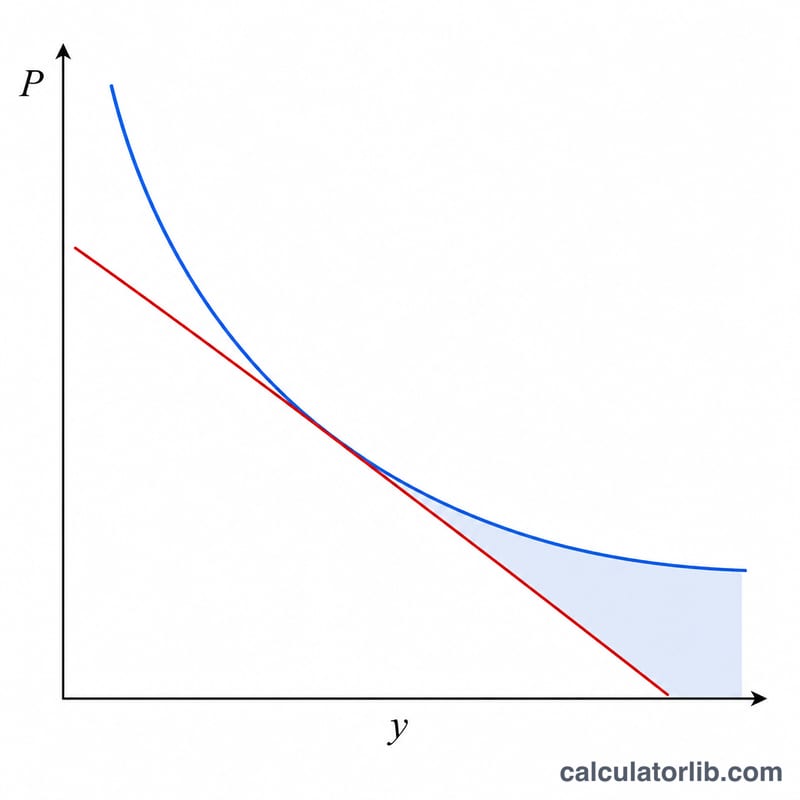

Interpreting Your Convexity Result

Convexity measures the curvature of a bond's price–yield relationship — how the bond's modified duration itself changes as yields move. It is the second-order term in the Taylor expansion of price with respect to yield, and it refines the straight-line estimate that duration alone provides.

The combined price-change approximation is:

$$\frac{\Delta P}{P} \approx -D \cdot \Delta y + \tfrac{1}{2}\, C \cdot (\Delta y)^2$$where \(D\) is modified duration, \(C\) is convexity, and \(\Delta y\) is the change in yield (in decimal form). The first term is the linear duration estimate; the second term is always positive for an option-free bond (because \(C>0\) and \((\Delta y)^2 \ge 0\)), so it adds to price when yields fall and softens the loss when yields rise.

Higher vs. lower convexity. A higher convexity number means the price–yield curve is more sharply bowed: the bond gains more when yields drop and loses less when yields rise than duration alone predicts. This asymmetry is generally desirable to a bondholder. A lower convexity means the price behaves more like a straight line — the duration estimate is more nearly exact, with smaller second-order benefit.

What raises convexity? All else equal, convexity increases with longer maturity (cash flows are spread further out and discounted more), with lower coupons (a larger share of value sits in the distant final payment — a zero-coupon bond has the highest convexity for its maturity), and with lower yields. It decreases with higher coupons and shorter terms.

Worked example. Suppose a bond has modified duration \(D = 7.0\) years and convexity \(C = 65\) years², and yields rise by \(\Delta y = 0.01\) (100 bp). The estimated price change is \(-7.0(0.01) + \tfrac{1}{2}(65)(0.01)^2 = -0.070 + 0.00325 = -0.06675\), or about −6.68% — roughly 0.33 percentage points less severe than the −7.00% duration-only estimate.

This explanation reflects standard fixed-income theory and is provided for educational purposes only; it is not investment advice.

Key Terms & Variables

- Face (Par) Value

-

The principal amount repaid to the bondholder at maturity, and the base on which the coupon is calculated. In the formula this is

face; \(1{,}000\) is a common convention. - Coupon Rate

-

The annual interest rate stated on the bond, applied to face value to determine the total annual coupon. Field

coupon, entered as a percent. - Yield to Maturity (YTM)

-

The single annual discount rate that equates the present value of all future cash flows to the bond's price — the bond's internal rate of return if held to maturity. Field

yield, entered as a percent. - Periodic Yield (\(y\))

- The yield per payment period: \(y = \dfrac{\text{YTM}/100}{k}\). All discounting in the convexity sum uses this per-period rate.

- Payments per Year (\(k\))

- The compounding/coupon frequency: 1 (annual), 2 (semiannual), 4 (quarterly), or 12 (monthly). It converts annual figures into per-period figures and sets the total number of periods \(n = \text{years}\times k\).

- Cash Flow (\(CF_t\))

- The payment received in period \(t\): the periodic coupon \(\dfrac{\text{face}\times\text{coupon}/100}{k}\) for each period, plus the face value returned in the final period \(t=n\).

- Duration

- The first-order (linear) sensitivity of price to yield — approximately the weighted-average time to receive cash flows, measured in years. It gives a straight-line estimate of price change.

- Convexity

- The second-order sensitivity — the curvature of the price–yield relationship. It corrects duration's straight-line estimate, especially for large yield moves.

- Convexity Units (years²)

- Because convexity is the second derivative of price with respect to yield (scaled by price), its natural units are time-squared, conventionally expressed in years². It is used in the \(\tfrac{1}{2}C(\Delta y)^2\) term of the price-change formula.

FAQ

Why is convexity always positive for plain bonds? Standard option-free bonds have positive convexity — price rises faster than duration predicts when yields fall.

What units is convexity in? This tool reports years². Multiply by \(\tfrac{1}{2} \times (\Delta y)^{2}\) to estimate the convexity contribution to a price change.

Does it work for zero-coupon bonds? Yes — set the coupon rate to 0 and the only cash flow is the face value at maturity.