What This Calculator Does

The Loan Term Comparison Calculator lets you put two repayment terms side by side — for example a 15-year vs a 30-year mortgage, or a 3-year vs 5-year car loan — using the same loan amount and interest rate. It shows the monthly payment, total interest, and total amount paid for each term, then highlights how much interest you save by choosing the shorter one. It works for any fixed-rate amortizing loan and is currency-neutral.

How to Use It

Enter the loan amount (the principal you borrow), the annual interest rate as a percentage, and two terms in years. Click calculate to see both scenarios. A shorter term usually means a higher monthly payment but far less interest over the life of the loan; a longer term lowers the monthly payment but increases total cost.

The Formula Explained

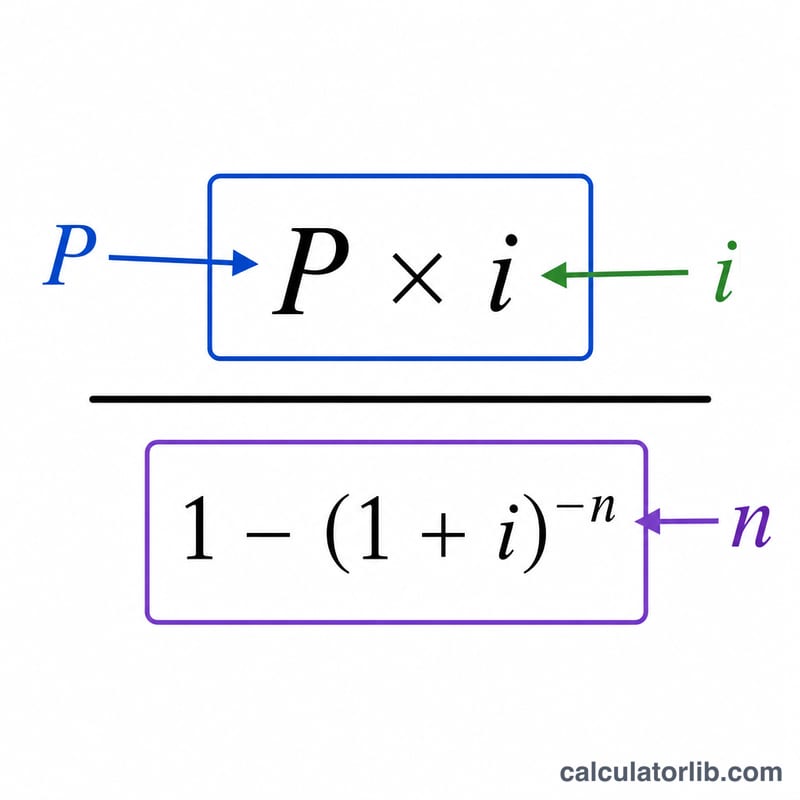

Each term uses the standard amortization payment formula: $$\text{PMT} = \frac{P \cdot i}{1 - (1 + i)^{-n}}$$ where P is the principal, i is the monthly interest rate (annual rate \(\div 12\)), and n is the number of monthly payments (years \(\times 12\)). Total interest is then \(\text{PMT} \times n - P\). The difference between the two total-interest figures is your savings.

Worked Example

Borrow $200,000 at 6% annual interest. Monthly rate \(i = 0.005\). For a 15-year term (\(n = 180\)), \(\text{PMT} \approx \$1{,}687.71\) and total interest \(\approx \$103{,}788\). For a 30-year term (\(n = 360\)), \(\text{PMT} \approx \$1{,}199.10\) and total interest \(\approx \$231{,}676\). Choosing the 15-year term saves about $127,888 in interest, though the monthly payment is about $489 higher.

FAQ

Why is a shorter term cheaper overall? You pay interest for fewer months and pay down principal faster, so less interest accrues.

Does this include taxes or insurance? No. It covers principal and interest only, so real-world mortgage payments may be higher.

What if the rate is 0%? The calculator divides the principal evenly across the months, so there is no interest in either term.