What the EAR Calculator Does

The Effective Annual Rate (EAR) calculator converts a quoted nominal (stated) annual interest rate into the true yearly rate you actually earn or pay once compounding is taken into account. Because interest charged or earned more often than once a year "earns interest on interest," the effective rate is always higher than the stated rate. This tool works for any investment, savings account, or loan worldwide — it is not country-specific.

The Inputs You Enter

- Annual rate (%) — the nominal or stated yearly interest rate (defaults to 6%).

- Compounding frequency — how often interest is applied. The calculator supports a wide range: annually (1), semi-annually (2), quarterly (4), bi-monthly (6), monthly (12), semi-monthly (24), bi-weekly (26), weekly (52), daily on a 360-day basis, daily on a 365-day basis, and continuous compounding.

Helpfully, the calculator displays the EAR for every compounding frequency at once, so you can compare options side by side.

The Formula

For a finite number of compounding periods n and nominal rate r (as a decimal):

$$\text{EAR} = \left(1 + \frac{r}{n}\right)^{n} - 1$$

For continuous compounding the calculator uses the exponential form: $$\text{EAR} = e^{r} - 1$$ Results are rounded to six decimal places and shown as a percentage.

Worked Example

Suppose you have a nominal rate of 6% compounded quarterly (\(n = 4\)):

- \(r = 0.06\), \(n = 4\)

- $$\text{EAR} = \left(1 + \frac{0.06}{4}\right)^{4} - 1 = (1.015)^{4} - 1$$

- $$\text{EAR} = 1.06136 - 1 = 0.06136$$ or about 6.1364%

So a 6% rate compounded quarterly truly yields 6.1364% per year. Compounded monthly it rises to about 6.1678%, and with continuous compounding to roughly 6.1837%.

Frequently Asked Questions

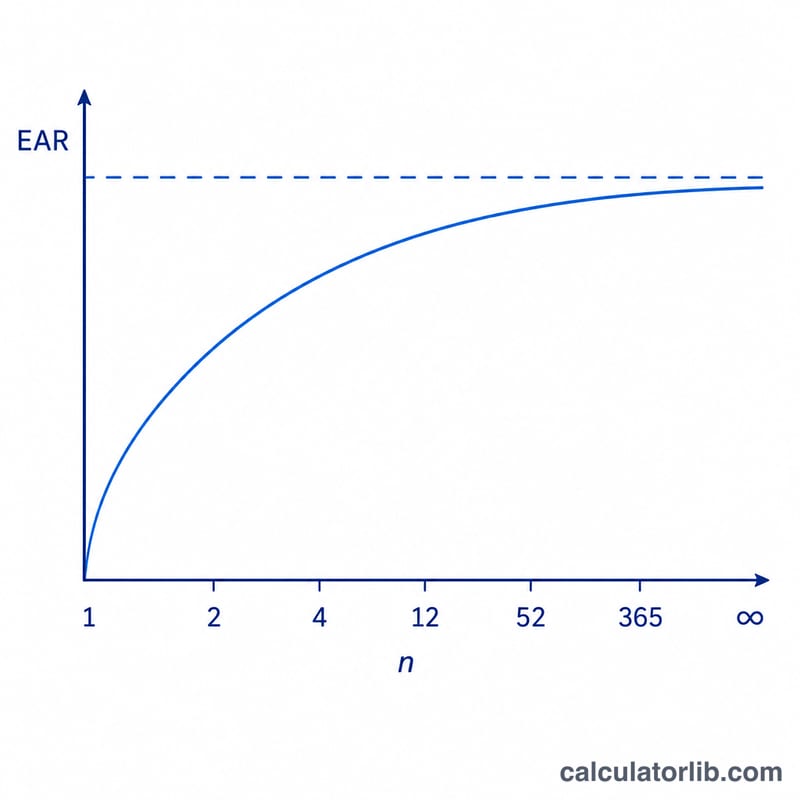

Why is EAR higher than the nominal rate? Because interest is added more than once per year and subsequent interest is calculated on the already-increased balance. The more frequent the compounding, the higher the EAR.

What does the 360 vs 365 daily option mean? Some institutions assume a 360-day year for daily compounding while others use the actual 365 days. The calculator shows both so you can match your lender's convention.

When should I use EAR? Use it to fairly compare loans or investments that quote different compounding frequencies — EAR puts them all on the same annual basis.